In Croatia in 2025, almost everyone faces the same dilemma: “What makes more sense – saving or investing?” Banks are still offering very low interest rates, while the prices of goods and services have risen by more than 4% compared to last year (HNB). This means that savers lose purchasing power every year, even if the number on their account stays the same. On the other hand, investing carries risk but creates the opportunity for your capital to work for you. In this article, we’ll look at where saving still makes sense, when investing becomes essential, and why the SPV joint investment model is one of the most practical answers for small and mid-sized investors.

Savings Still Make Sense – But Only as a Safety Net

Savings are not useless—quite the opposite. They are the foundation of every financial plan. The standard rule says everyone should keep an “emergency fund” – enough money to cover 3–6 months of basic expenses. That money must be safe and easily accessible, without exposure to fluctuations. Bank accounts or time deposits are perfect for this purpose.

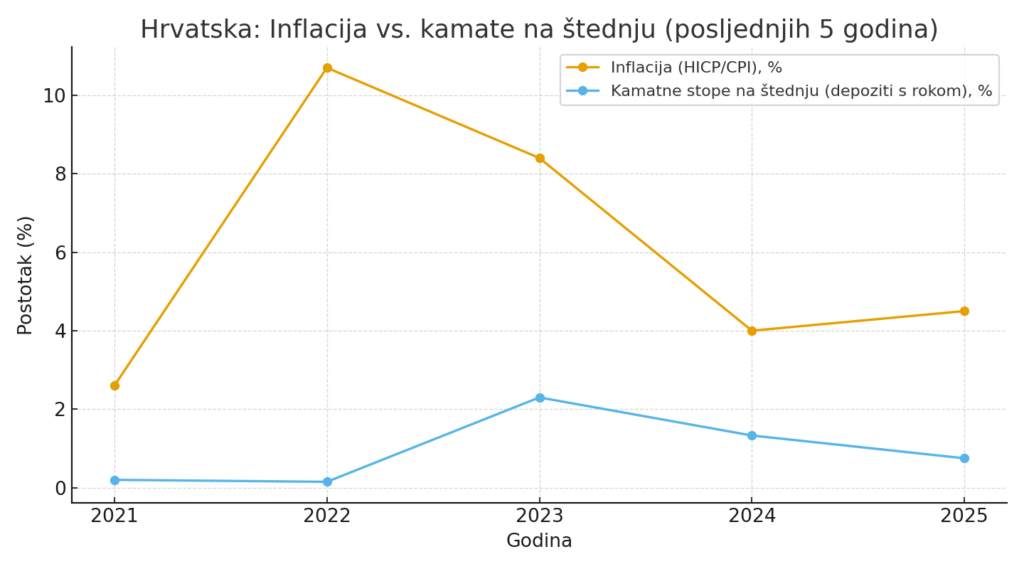

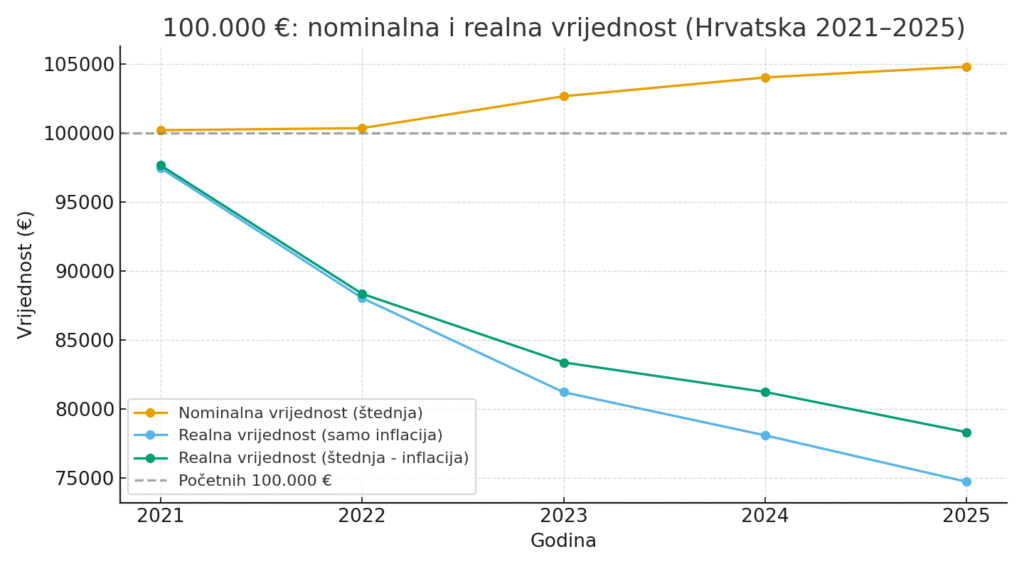

The problem begins when you keep amounts beyond that in a savings account for years. Example: with a 1% deposit rate and 4% inflation, you are effectively losing about 3% of purchasing power every year. Over 10 years, your money may lose up to 30% of its value. The account balance looks the same—or slightly higher—but what you can buy with it is much less.

This is not just a Croatian problem. Similar trends have been seen in Germany and Austria, where rates were near zero for years. But in Croatia, the effect is sharper because people traditionally prefer to keep their wealth in banks. According to HNB data, households still hold billions of euros in savings accounts, even though that wealth is shrinking in real terms.

So, yes to savings—but only up to the safety net. Everything above that needs a smarter plan.

Why Investing Becomes Necessary

If you want your capital to maintain or increase its value, investing is unavoidable. Investing means taking on a certain level of risk in exchange for the potential of higher returns. This is the key difference between a saver and an investor: a saver hopes the bank will protect value, while an investor actively seeks to grow their wealth.

The biggest beginner’s mistake? Waiting for the “perfect moment.” Many believe the right project will magically appear, or that markets will crash and they’ll “jump in.” But statistics show long-term consistency beats market timing. By investing regularly and reinvesting profits, the effect of compounding works in your favor.

Where to invest? Stocks, bonds, gold, cryptocurrencies… but for most conservative Croatian investors, the natural answer is real estate. Why? Because it’s a tangible asset you can use, rent, or sell. Property prices in Zagreb and on the coast have risen steadily over the last five years, with demand still strong, especially in tourist regions.

Investing isn’t a “luxury for the rich.” It’s the only way to protect the value you’ve built and give yourself more options long-term—whether through rental income or appreciation of the property itself.

Real Estate and the SPV Model – Investing Without Middlemen

Traditional crowdfunding platforms act as middlemen: they gather third-party projects, present them to investors, and take a commission. This often creates misaligned interests between the platform and the investor.

The SPV model works differently. A separate company (SPV – Special Purpose Vehicle) is founded, which directly owns the property. Investors and the project team enter together, and ownership shares are defined proportionally to invested capital. If you invest 10%, you own 10% and receive 10% of the project’s profits. Earnings may come from rental income or profit upon sale.

The advantage is transparency and equality. There’s no middleman—everyone shares the same goal: project success. This eliminates the common problems early crowdfunding platforms faced: poor-quality projects, high fees, and lack of control.

Investing isn’t a “luxury for the rich.” It’s the only way to protect the value you’ve built and give yourself more options long-term—whether through rental income or appreciation of the property itself.

How to Invest Smaller Amounts and Build a Portfolio

The most common myth about real estate is: “You need hundreds of thousands of euros.” The truth is the opposite. Today you can start with much smaller amounts.

Imagine this example: you invest €5,000 in an SPV project that develops a holiday villa. Your share is proportional, for example 5% of the project. When the villa begins generating rental income, you receive 5% of the net revenue. If it is sold after a few years, you receive 5% of the profit. Most importantly, that return can be reinvested into new projects.

This means that over time you can build a portfolio of shares in several properties. You are not tied to a single apartment, you do not need to take out a loan, and you do not need to deal with tenants or repairs. Instead, your capital works quietly in the background while you decide which projects to join.

This approach allows the power of compounding to work for you. The point is not to earn once and spend, but to invest regularly and reinvest the profits. Small amounts, when distributed wisely and consistently reinvested, can grow into serious wealth within a few years. That is what separates a passive saver from an active investor.

Diversification and Security

Anyone who invests knows one rule: never put all your eggs in one basket. Diversification is the way to protect capital and reduce risk.

In real estate, that means spreading funds across several projects. Instead of putting all your money into one apartment in Zagreb, you could join three different SPVs: one rental apartment in Zagreb, one villa on the coast, and one house in a smaller town. This reduces dependence on a single market or project. If prices fall in Zagreb, the tourist season on the coast may lift the portfolio into profit.

In addition, the SPV structure ensures clear legal protection. The property is owned by the company, and you are the owner of a share in that company. Profits are distributed proportionally, and everything is managed transparently through business records. Extra security also comes from EU regulation (ECSP 2020/1503), which standardizes rules for this type of investment and strengthens investor protection.

Diversification does not mean avoiding risk. It means managing risk wisely. In today’s conditions, that is the best way to sleep peacefully while your capital works for you.

Conclusion

Savings remain essential as a safety net. But everything above that loses value over time if left in a bank account. Investing, especially in real estate through SPV models, gives you the opportunity to:

-

- Preserve and grow the value of your capital

- Participate in real projects

- Earn income without loans and without managing tenants

If you want your money to truly work for you, it is time to take a step beyond savings.